![]()

Kerrigan Advisors today released the results of its fourth annual OEM survey, providing unique, and not often public, insights into the perspectives of US automotive manufacturer executives. Reflecting a strong outlook for US automotive retail among OEMs, the 2026 Kerrigan OEM Survey reveals that OEMs are increasingly seeing AI as a profitability driver at the retail level, as they navigate softening new vehicle sales and absorb the lion’s share of tariffs, all while maintaining confidence in dealership blue sky values and expecting a very active buy/sell market in the year ahead.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260707469261/en/

Automotive OEMs Expect AI to Lift Dealership Profitability

“The story of this year’s survey is that OEMs see the economics of the dealership model getting stronger, not weaker,” said Erin Kerrigan, Founder and Managing Director of Kerrigan Advisors. “They expect AI to increase future dealership profitability, and they plan to shoulder the bulk of tariff costs themselves rather than pass them to their dealers. That combination of rising dealer productivity and sustainably higher retail vehicle margins helps explain why OEMs project blue sky values to hold firm, or increase, even as vehicle prices climb and vehicle sales rates flatten.”

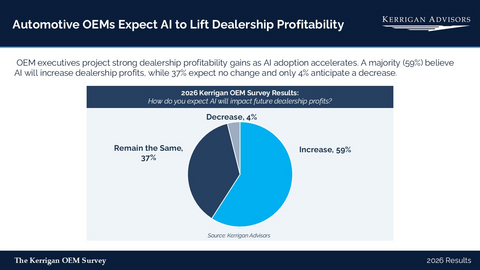

OEMs Expect AI to Increase Dealership Profits

For the first time, Kerrigan Advisors asked OEM executives how they expect AI to affect future dealership profits, and the results were decisive: 59% believe AI will increase dealership profits, while 37% expect no change, and just 4% anticipate a decrease. The finding is reinforced by the 2025 Kerrigan Dealer Survey, in which 90% of dealers reported they are already using or plan to use AI in their operations, indicating that the operational adoption needed to realize those gains is already underway. Kerrigan Advisors expects wide-scale AI deployment to reduce selling expenses and lift revenue per employee, boosting dealer productivity and profitability.

“AI is moving from experiment to infrastructure in the dealership,” said Ryan Kerrigan, Managing Director of Kerrigan Advisors. “When OEMs and dealers alike expect it to lower operating costs and raise revenue per employee, that’s a structural improvement to the profitability of the business, and a meaningful part of why we project future dealership earnings and blue sky values to stay strong.”

Buy/Sell Activity and Blue Sky Valuations Reflect OEM Confidence

For the first time, Kerrigan Advisors asked OEM executives about their expectations for dealership buy/sell activity, and the results are compelling: 88% of OEM executives expect buy/sell activity to accelerate or hold steady – consistent with the record activity recently reported in Kerrigan Advisors’ recent Blue Sky Report®. Over a third (35%) are anticipating more buy/sells for their franchises, while 53% expect activity to continue at today’s elevated level.

Dealership valuation expectations reflect similar confidence: 82% of OEM executives expect dealership blue sky values to increase or remain the same, with 21% anticipating an increase and 61% projecting no change. Just 18% expect a decrease, versus 22% in 2025, a four-percentage-point improvement.

Fewer, Larger Dealers as Networks Consolidate and Facility Standards Rise

The survey results also reveal that OEM executives increasingly envision a dealership network of fewer, larger and better-capitalized retailers. Those who expect fewer dealers in their network in the next five years increased 12 percentage points, to 45% from 33% in 2025, while only 14% expect to add dealers. This reflects the industry’s long-term consolidation trajectory, with buy/sell activity now pacing at roughly double its pre-pandemic level. Rising facility standards are also accelerating that dynamic, with 43% of OEM executives indicating their organization will require a new image facility within five years.

“The consolidation signal in this year’s survey is significant: OEMs are planning for a network of fewer, but more profitable, dealers,” said Erin Kerrigan. “For well-capitalized operators, this is a market that continues to reward scale and investment, and it’s a major reason buy/sell activity and valuations are expected to stay strong, as leading consolidators seek growth.”

Tariffs Soften New Vehicle Sales Outlook; Long-Term EV Sales Growth Projected

Sentiment towards new vehicle sales softened this year. The percentage of OEMs projecting a decline in sales rose to 23% from 18% in 2025 – while those expecting an increase fell to 25% from 36%.

The softening sales outlook is closely tied to tariffs, and OEM executives were clear about where the cost will land: not on their dealers. A majority (58%) expect OEMs to bear the majority of US tariff costs and 37% expect those costs to fall to consumers, while just 5% expect dealers to be the primary absorbers. As OEMs realize the expense of tariffs, they are likely to both increase vehicle prices and scale back consumer incentives that support demand, a key driver of this year’s weaker sales sentiment. Tariff assumption by the OEMs also helps reconcile two conflicting trends unfolding at once: new vehicle prices are rising and affordability is declining, yet dealership values are expected to hold firm or increase because dealer profitability is largely insulated from direct tariff pass-through expense.

Interestingly, despite tepid EV sales and the elimination of both the federal EV tax credit and the CARB EV mandate during the survey period, OEMs show no signs of retreating from electrification. OEM executives surveyed expect that EVs will represent an average of 21% of their sales in five years – more than double current US EV market share. This positive projection is likely underpinned by their massive investment in EV development and production capacity, as well as China’s rising influence on the global automotive industry.

“Tariffs introduced real uncertainty into the new vehicle sales outlook, and that shows up clearly in the data,” said Ryan Kerrigan. “But the more telling finding is who will absorb the cost – and OEM executives are not pointing at dealers. That distinction matters for dealership profitability, and it helps explain why valuations and transaction activity are projected to hold firm even in a more complicated sales environment.”

Key 2026 Kerrigan OEM Survey Data

- 88% of OEM executives expect buy/sell activity to hold steady or accelerate over the next 12 months, 35% expect more transactions and 53% expect activity to continue at today’s elevated level.

- 82% of OEM executives expect dealership blue sky values to remain the same or increase in 2026; only 18% expect a decrease, a four-percentage-point improvement from 2025.

- 59% of OEM executives believe AI will increase dealership profits, 37% expect no change and just 4% anticipate a decrease.

- 45% of OEM executives expect to have fewer dealers in their network in five years, a 12-percentage-point increase from 33% in 2025.

- 31% of OEM executives project an increase in dealer facility requirements over the next five years, up six percentage points from 25% in 2025; 43% say their organization will require a new image facility of their dealers within five years.

- 86% of OEM executives expect dealers to either lead or share in managing customer relationship and data over the next five years.

- Planned use of ROFR (right of first refusal on a buy/sell) declined sharply. Just 8% plan to ROFR more than 25% of transactions, down from 28% in 2025; 14% do not intend to ROFR any transactions.

- 77% of OEM executives expect new vehicle sales to remain flat or rise over the next 12 months, though the share projecting a decline rose to 23%, up from 18% in 2025.

- 58% of OEM executives expect OEMs to bear the majority of US tariff costs; 37% expect consumers to absorb most of the burden; just 5% expect dealers to be primary absorbers.

- 38% of respondents project a 30-60 days’ supply of new vehicle inventory over the next 12 months, up 11 percentage points from 27% in 2025.

- 56% of OEM executives expect new vehicle gross margins to normalize back toward pre-pandemic levels, up eight percentage points from 48% in 2025.

- On average, OEM executives expect EVs to represent 21% of their sales within five years, more than double the ~8% EV market share in the US in 2025.

Methodology

The data for The Kerrigan OEM Survey was gathered from Kerrigan Advisors’ annual survey of automotive OEM executives in conjunction with the issuance of The Blue Sky Report®. The survey is based on 150+ responses from OEM executives in Kerrigan Advisors’ proprietary database. Responses were collected from December 2025 to June 2026.

- To download the full Kerrigan OEM Survey report, click here.

- To download a preview of The Blue Sky Report®, published by Kerrigan Advisors, click here.

- To access The Kerrigan Index™, click here.

- To access results from the latest Kerrigan Dealer Survey, click here.

About Kerrigan Advisors

Kerrigan Advisors is the leading sell-side advisor and thought partner to US auto dealers. Since its founding in 2014, the firm has led the industry with the sale of 450 franchises generating more than $10 billion in client proceeds, including two of the largest transactions in auto retail history – the sale of Jim Koons Automotive Companies to Asbury and Leith Automotive to Holman. The firm advises the industry’s leading dealership groups, enhancing value through the lifecycle of growing, operating and, when the time is right, selling their businesses. Led by a team of veteran industry experts with backgrounds in investment banking, private equity, accounting, finance and real estate, Kerrigan Advisors is the only firm in auto retail exclusively dedicated to sell-side advisory, providing its clients with the assurance of a conflict-free approach. View all of Kerrigan Advisors’ recent transactions here.

Kerrigan Advisors monitors conditions in the buy/sell market and publishes an in-depth analysis each quarter in The Blue Sky Report®, which includes Kerrigan Advisors’ signature blue sky charts, multiples, and analysis for each franchise in the luxury and non-luxury segments. To download a preview of the report, click here. The firm also releases monthly The Kerrigan Index™ composed of the seven publicly traded auto retail companies with operations focused on the US market. The Kerrigan Auto Retail Index is designed to track dealership valuation trends, while also providing key insights into factors influencing auto retail. To read the 2025 Kerrigan Dealer Survey, click here. To read the 2026 Kerrigan OEM Survey, click here. Kerrigan Advisors is also the co-author of NADA’s Guide to Buying and Selling a Dealership. Additionally, Kerrigan Advisors publishes a podcast, Beyond Blue Sky – A Kerrigan Conversation, where Kerrigan Advisors’ clients and industry leaders share the mindset, strategy and personal stories behind a once-in-a-generation transaction.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260707469261/en/

Media gallery